You've probably heard of share buybacks at some point or another. Businesses theoretically utilize share buybacks to transfer profits to investors. It certainly sounds like a relatively simple mechanism just from the name.

While Share Buybacks can benefit shareholders, they can also have a significant impact on investors. It's a great and generally effective way for a business to distribute its profits to its investors, but in some cases, it actually reduces shareholder value and can be used to manipulate accounting data to increase executive pay. Clearly, it's a more complicated and controversial topic than you might have expected. In fact, we've even seen American banks banned from carrying out buybacks by the US Federal Reserve during this pandemic.

What is the Share Buyback? What does it mean for investors, and is it a good or a bad thing?

A Share Buyback occurs when a corporation rebuys its shares on the open market. Although there is a little more to it, the process itself is quite simple because businesses generate money all year. To use some of the extra cash to buy their own stock, they can make a tender offer to entice interested shareholders to sell their shares for a predetermined price.

They might simply go to the market and place buy orders on their own ticker at this time, similar to other investors. This is distinct from the management of the company purchasing stock. Executives may amass shares of the company they manage by making investments with their own money or by receiving compensation from their corporation.

The shares from a buyback are not going to any individual's personal investment account, but instead, the shares purchased through a buyback are actually absorbed by the company and cease to exist. In other words, a buyback removes shares from the market as a whole, reducing the total number of outstanding shares that investors can now buy or sell.

Why would a company do this?

Eliminating shares may not appear to be very productive and it significantly increases the percentage of the company owned by other shareholders. After all, each year represents a fraction of a corporation's ownership, and by reducing the total number of outstanding shares, the company increases the stake of the remaining investors.

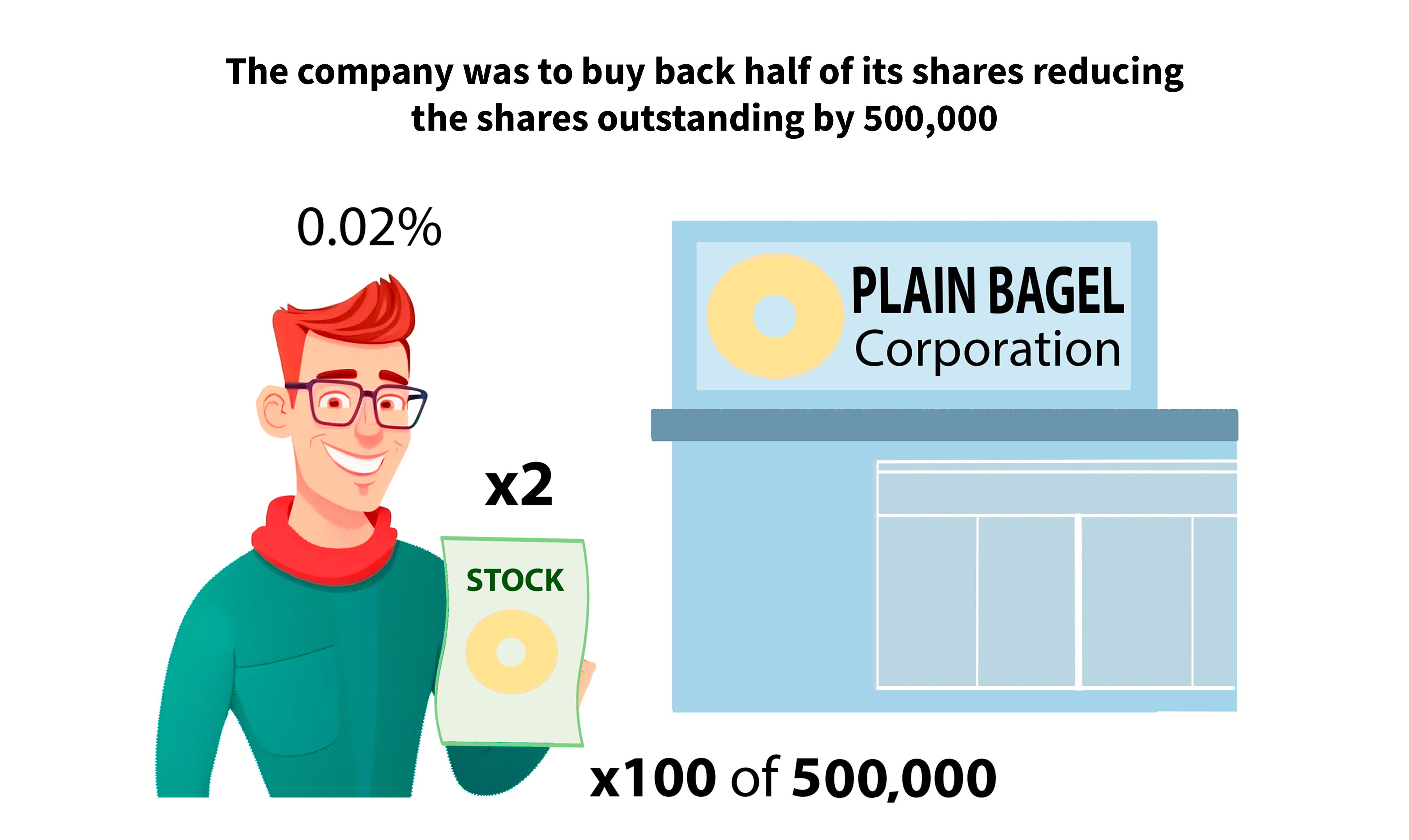

For example, imagine you're an investor who owns 100 shares of plain bagel co the company has a total share outstanding count of 1 million shares. So you currently own 0.01 of the firm now.

Imagine the company was to buy back half of its shares reducing the shares outstanding by 500,000.

All of a sudden, you as a shareholder now own zero point zero two percent of the company. It might not sound like a lot but you've doubled your ownership of plain bagel co with fewer shareholders laying claim to the company. Your share of the pie has now increased.

Even while it may not appear to be so, this procedure is actually quite comparable to a business paying off its debt because equity isn't really a liability. The company is in effect paying off existing investors so that they relinquish their claim over the firm which reduces the number of people who control the company. However, a firm will only repurchase its shares if it has no other plans for the money. If a company has the opportunity to invest in a project that will double operations, it may keep the money to expand its business in the same way and it might be a good idea for them to take out a fairly low-interest loan.

If they're instead more mature and don't really stand to benefit from an extra manufacturing plant or sales outlet, then a buyback is an effective way for them to transfer their profits to shareholders rather than blowing the money on some unnecessary venture.

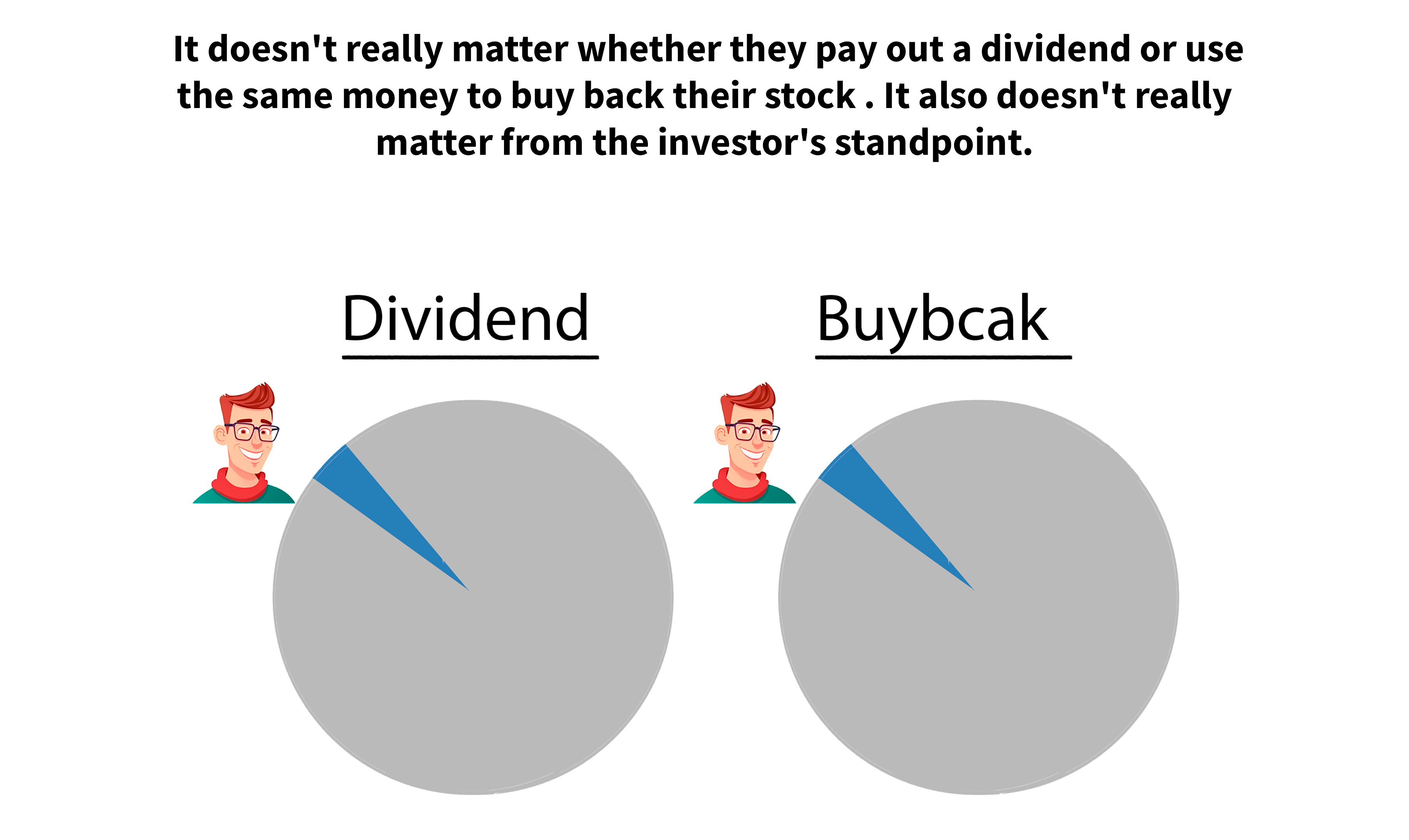

You might be thinking that this sounds a lot like a dividend, which is when a company pays some of its profits directly to investors, it doesn't have a better use for the money and you'd be exactly right. In fact, from the standpoint of the corporation, share repurchases are regarded as being identical to a dividend under certain assumptions. It doesn't really matter whether they pay out a dividend or use the same money to buy back their stock because both involve taking their after-tax profits and giving the money to their investors. It also doesn't really matter from the investor's standpoint.

If they receive the dividend and decide to reinvest it back into the company, then the result is nearly identical to the outcome of the buyback.

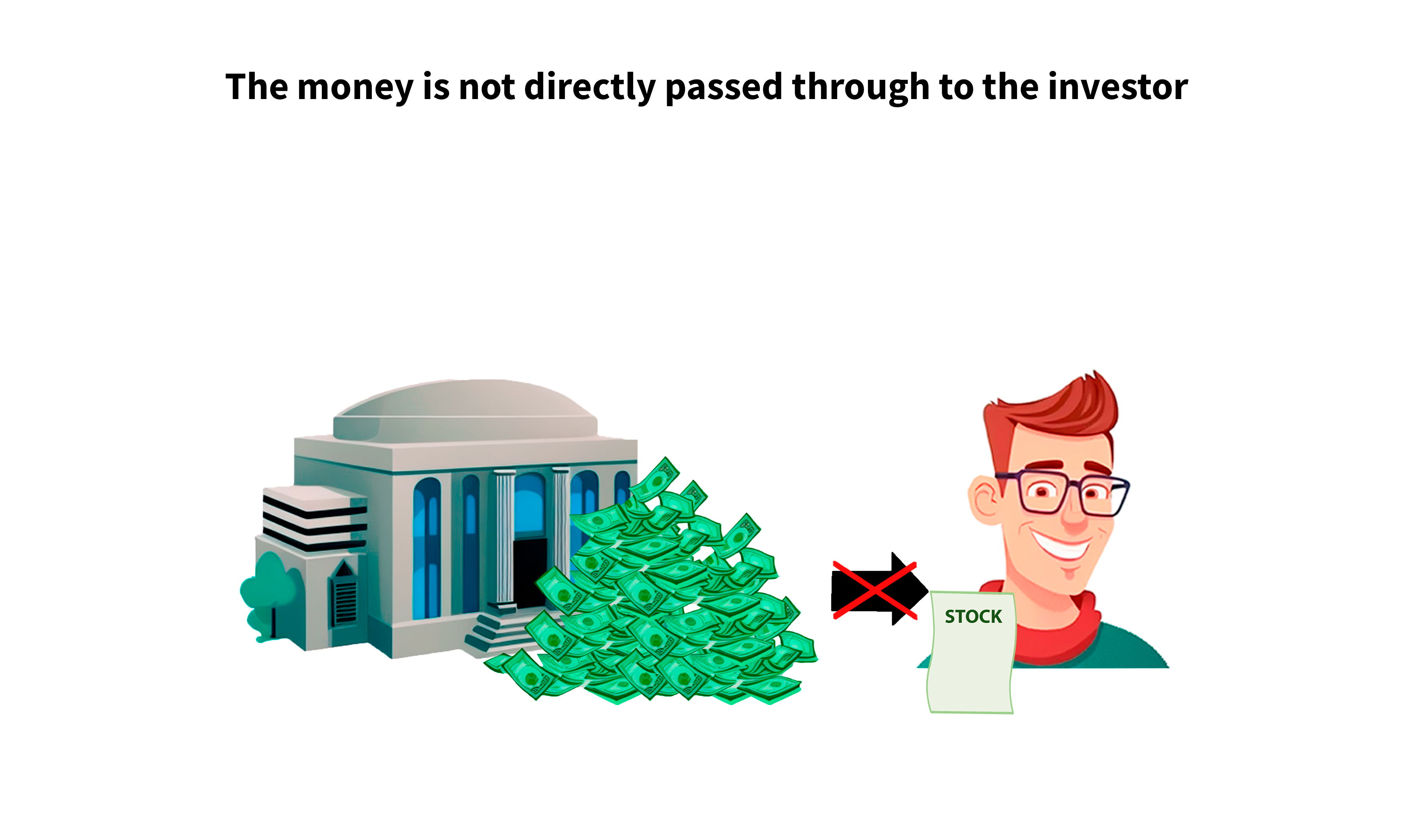

In fact, when you consider taxes, buybacks actually have a bit of an advantage over dividends after all experience in double taxation. When the company earns a profit, the money is first taxed at the corporate level. When it is later received as income through a share repurchase, it is taxed at the investor level but the money is not directly passed through to the investor.

They can obtain a comparable benefit without immediately incurring personal income tax. You can see why many investors enjoy share repurchases, but their advantages go beyond the increase in the number of shares purchased. They also enhance a company's financial ratios and its earnings per share, a crucial indicator of a stock's profitability.

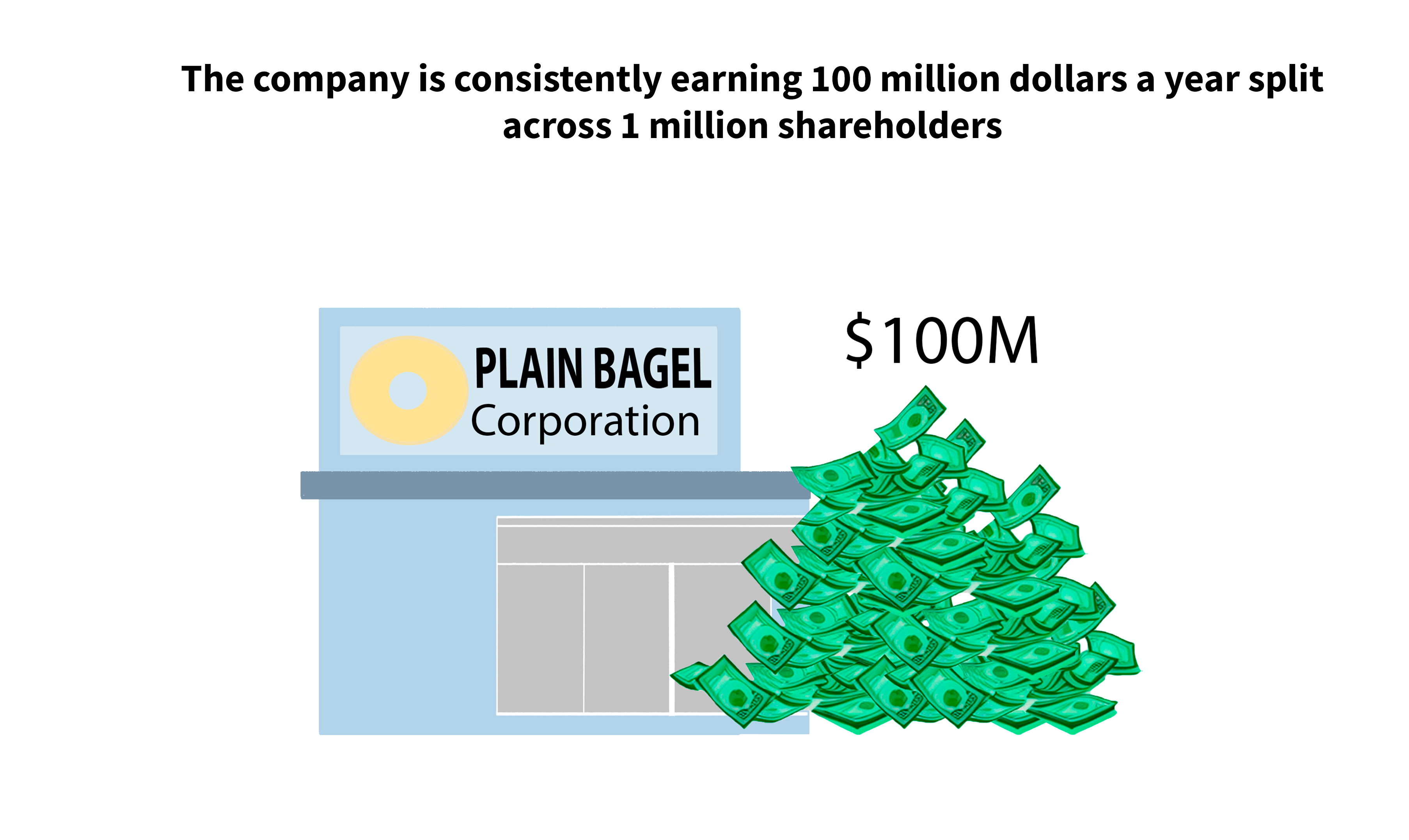

For example, with plain bagel co, imagine that the company is consistently earning 100 million dollars a year split across 1 million shareholders.

The stock has Earnings Per Share of 100 after carrying out the buybacks. However, this would increase to 200 a share the company hasn't earned any more money but with fewer people to split the profits across their earnings per share have now doubled.

Finally, there's actually some evidence that share buybacks can boost the stock's price. Not only is the company, but now inserting itself into the market as a buyer for its share which as supply and demand dictates will increase the price. Buybacks are viewed as a positive signal and they are often interpreted as a positive sign that operations are going well. After all, management buying back their shares sort of implies that the company has enough cash to spend and that management believes that the stock is a good investment

A buyback can be a sign of a diligent management team returning capital to their shareholders in a fairly efficient manner, but in other circumstances, it can actually be a waste of money. In some cases, it can even be used for more devious purposes to start off. Share buybacks are really only beneficial when the stock's price is undervalued. As you know, investors are always looking to buy low and sell high in practice. We want the companies that we have our money in to follow that same mentality. A company should only buy back its stock when it believes that the stock price is undervalued and lower than what it should be.

For example, imagine you had two identical companies with 100 million shares outstanding.

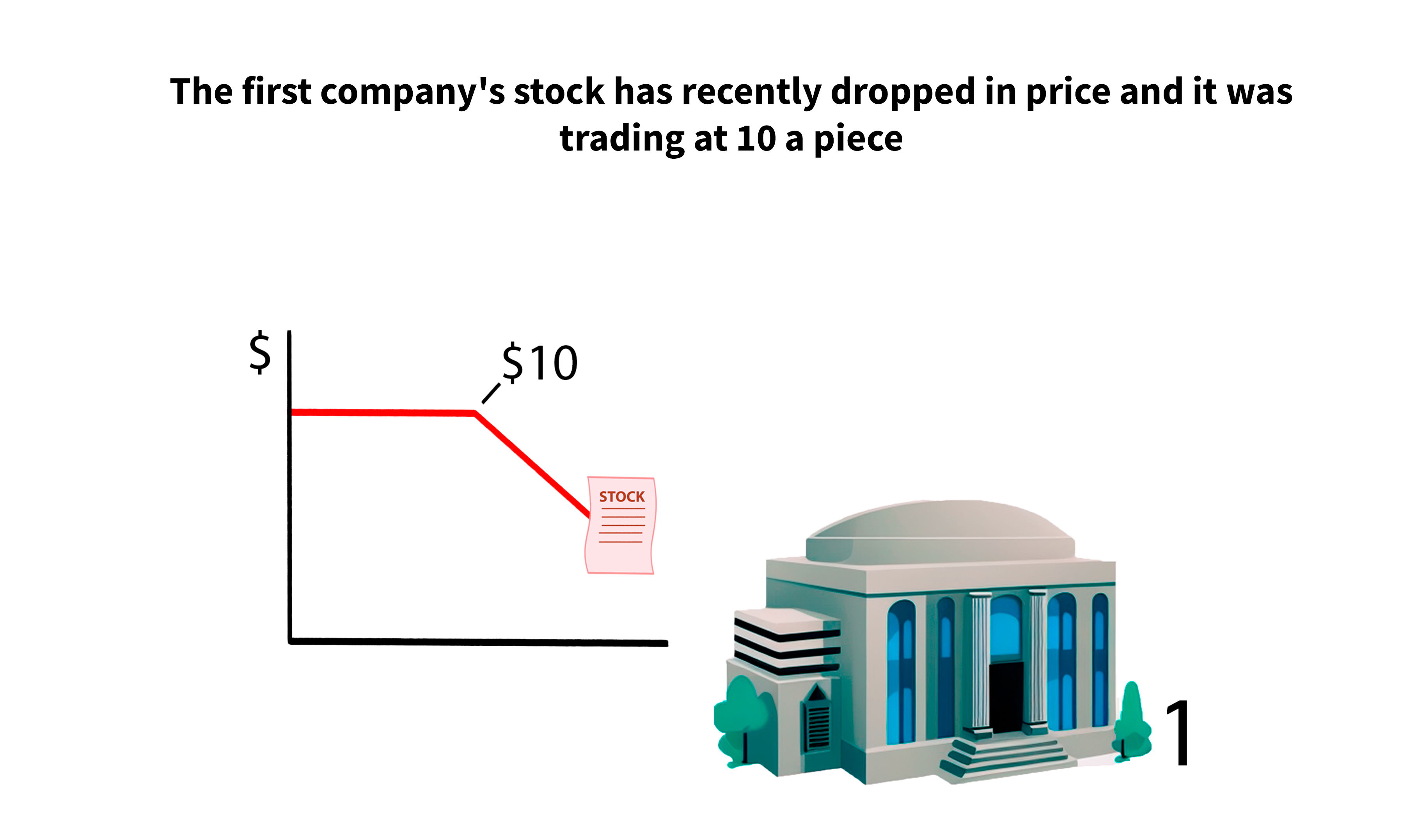

The first company's stock has recently dropped in price and it was trading at 10 a piece.

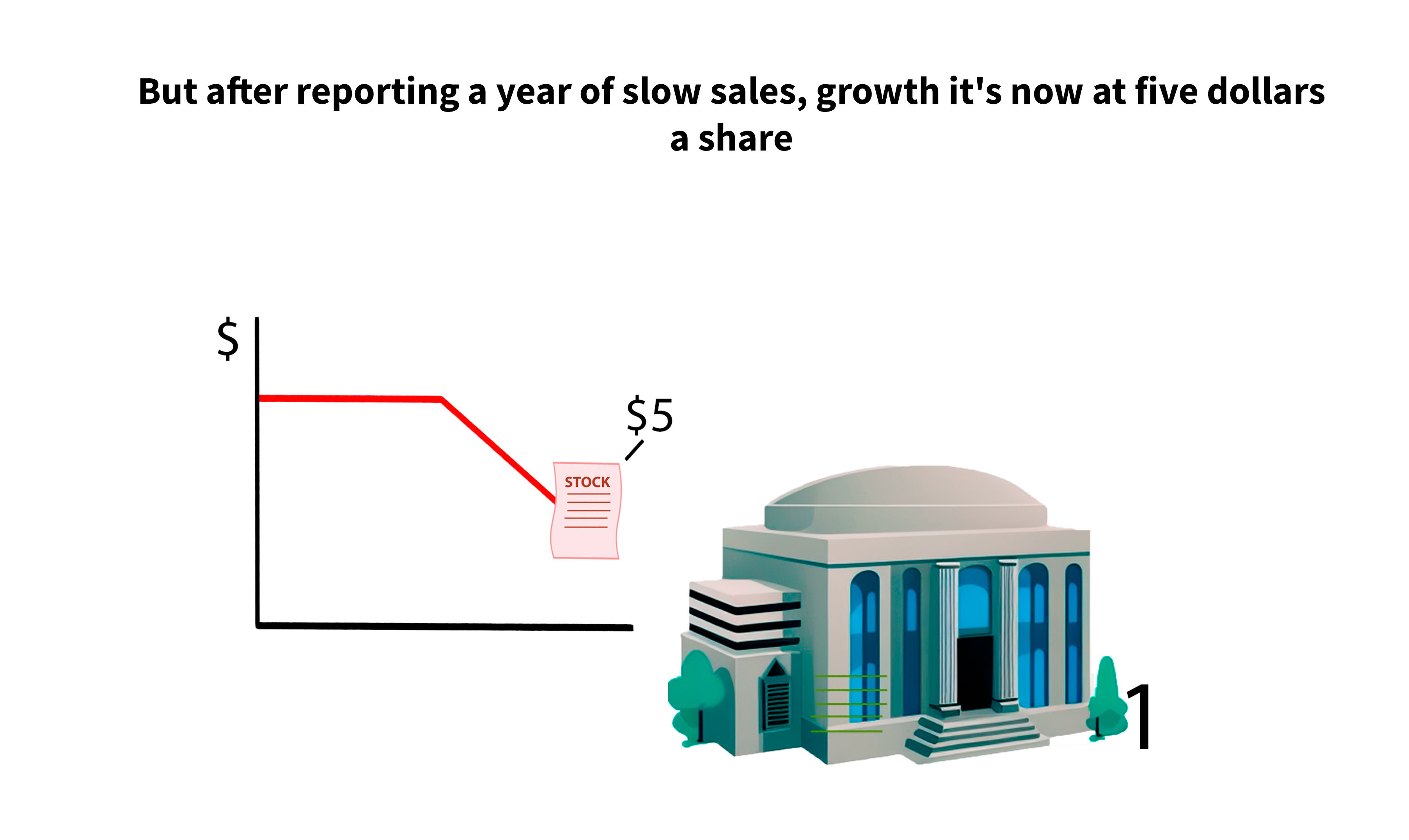

But after reporting a year of slow sales, growth it's now at five dollars a share.

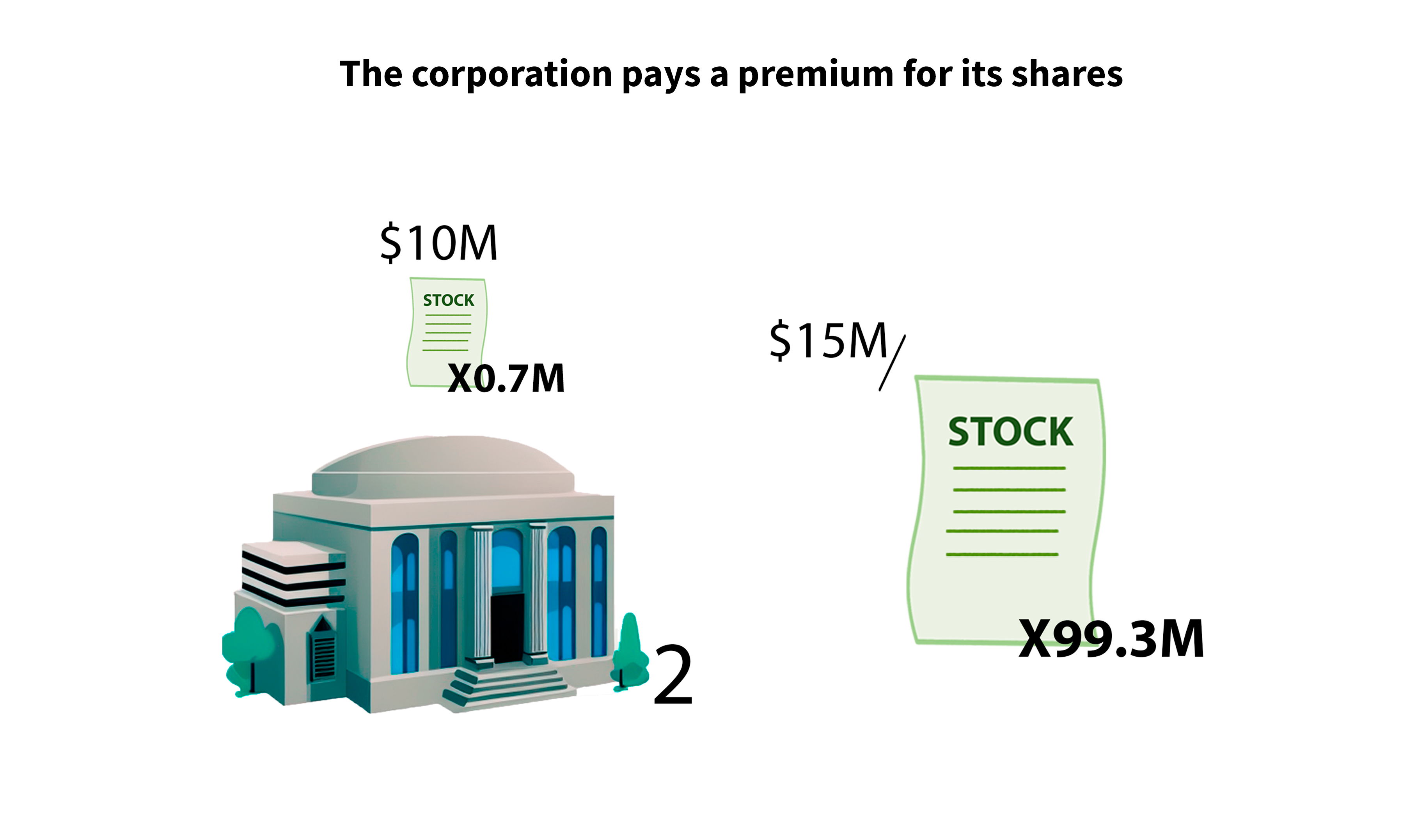

Meanwhile, the second company has had an abnormally strong year and its stock price has increased from ten dollars to fifteen dollars. If both companies want to carry out a share buyback of 10 million dollars, you'll see that the impact varies pretty drastically for the first company. Since the stock price is so low, management is able to buy back two million shares reducing their shares outstanding by two percentage points. It is a pretty good result for Romanian investors for the second company.

The corporation pays a premium for its shares so the overall buyback has a lower impact on reducing the share count. The same amount of money can only be used to repurchase about 0.7% of the outstanding shares.

Even after their stock price has increased for a while, we frequently observe firms buying back shares. This may reflect management's confidence that the business has much more room to run, but sometimes, companies will simply carry out share buybacks because investors have come to expect them, and pulling back now could hurt the stock's price by providing a negative signal to investors. With some assuming that management is now less confident than they used to be, management may also simply be overconfident believing there's nowhere to go but up even if the fundamentals don't really justify that buyback. Sadly, management will sometimes carry buybacks out of self-interest.

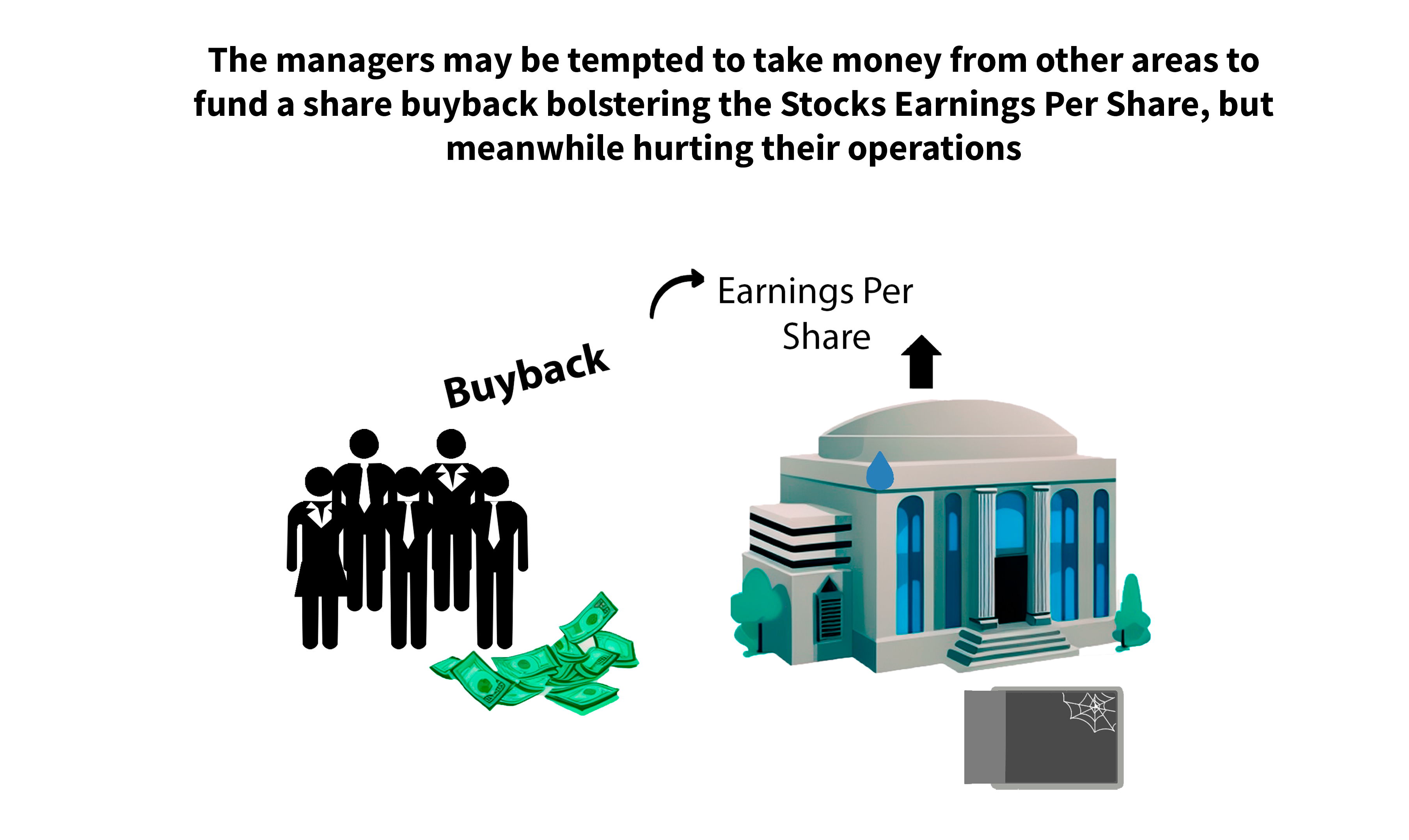

Imagine, for example, that a management team has its compensation tied to their company's earnings per share, and in a given year, the company sees its net income fall. The company is strapped for cash and really isn't well equipped to carry out a share buyback, but a buyback could boost eps to the point where management reaches their growth target and unlocks bonus compensation.

The managers may be tempted to take money from other areas to fund a share buyback bolstering the Stocks Earnings Per Share, but meanwhile hurting their operations just to unlock these special bonuses that they clearly don't deserve. This is part of the reason why we saw the Federal Reserve ban banks from carrying out buybacks in the US. There was concern that the banks would put money towards buybacks that should be going towards other activities such as building a rainy day fund.

Nonetheless, for value investors share buybacks are sort of viewed as a broadly positive thing if you like a company and think it's undervalued then why wouldn't you want to see your stake in the company increase there are other factors you need to consider in some investment theory even argues that share buybacks are a moot point for investors so while you might like to see a company's share count declining make sure the company is justified in its action.

If you want to gauge a company's buyback activity, you can check out its cash flow statement where you'll see how much money the company has spent or alternatively raised by buying or selling its own shares.

We should also view the share buybacks in conjunction with the company's balance sheet strength and their stock's valuation to ensure that it makes sense for the business. As with most things in investments, not all that glitters is gold and there's no clear-cut rule when it comes to Share Buybacks. Even as a value investor, the client share count can be a very wonderful indicator to view, but I would much prefer to invest my money in a corporation that is reducing its share ownership for a good cause than one that is purchasing package shares for a terrible one.

Stock buybacks are just an example of one of those concepts that while important to the investor aren't that widely understood. The truth is, if you're going to pick and choose your own stocks, you need to understand the intricacies of the investment vehicle, business, and economy.

Key Takeaways:

1. Companies can transfer earnings to shareholders through stock buybacks, but they also have the potential to depress shareholder value and tamper with accounting data.

2. In a share buyback, a company purchases its own stock on the open market, lowering the total number of outstanding shares that are available for purchase or sale by investors.

3. Share buybacks can increase the percentage of the company owned by other shareholders, and they can also enhance a company's financial ratios and earnings per share.

4. Share buybacks are beneficial when the stock's price is undervalued, and they can be a sign of a diligent management team returning capital to their shareholders.

5. Share Buybacks may be carried out for malicious objectives like boosting CEO compensation or stock price growth.

6. Investors should consider a company's balance sheet strength and stock valuation when evaluating share buybacks.